Audit evidence is the information or documentation that auditors gather and evaluate during the audit process to form an opinion about the fairness of the financial statements or the effectiveness of internal controls in an organization.

This evidence serves as the foundation for the auditor’s conclusions and opinions. Audit evidence can take various forms, including documents, records, observations, confirmations, and more. It is crucial for auditors to obtain sufficient and appropriate evidence to support their findings and conclusions.

Auditors often grapple with vast troves of data in their quest for the quintessential proof, akin to finding a needle in a haystack. Moreover, the burden rests on them to ensure no critical elements are omitted.

Audit evidence functions as the lodestar that steers auditors in rendering their verdict on a company’s financial well-being or the efficacy of its internal controls. Investors and stakeholders rely on these appraisals to make judicious decisions.

With this groundwork laid, let us proceed to explore precisely why audit evidence plays such a pivotal role.

Why is audit evidence important?

Audit evidence serves as the cornerstone of the auditing process, playing a pivotal role in assessing compliance, ensuring reliability, and forming independent opinions on an organization’s adherence to regulations. It is the basis for determining whether compliance statements accurately represent an organization’s compliance posture and performance, encompassing its conformity with specific laws, regulations, policies, and procedures.

Furthermore, compliance audit evidence is instrumental in establishing whether an organization operates within the boundaries set by both external regulations and internal guidelines. Beyond the auditing realm, it instills trust in the organization’s responsibility and commitment to upholding these rules, a crucial factor in ensuring safety and fairness for all stakeholders.

The International Standards on Auditing (ISA) 500 highlights the significance of audit evidence as the information upon which auditors base their conclusions to formulate an audit opinion. In tandem, the Institute of Internal Auditors (IIA) Standard 2330 defines quality evidence as information that is sufficient, reliable, relevant, and useful in achieving the engagement’s objectives.

In this context, auditors face the intricate task of requesting, gathering, and appropriately storing documentation. While the structure and format of work papers may vary among organizations and engagement types, it is essential to maintain consistency in documentation practices, adhering to best practices throughout the audit process.

How does audit evidence help?

Audit evidence plays a central role in the audit process, and its importance can be summarized in several key points:

1. Verification of financial statements

Audit evidence is used to verify the accuracy and completeness of the financial statements presented by an organization. It helps determine whether the financial information fairly represents the entity’s financial position, performance, and cash flows.

2. Supporting audit opinions

The auditor’s ultimate goal is to express an opinion on the financial statements. Audit evidence is the basis for forming this opinion. The type and quality of evidence obtained influence the level of confidence the auditor can have in their conclusions.

3. Risk assessment

Audit evidence is essential for assessing and addressing the risk of material misstatements in financial statements. Auditors use evidence to identify areas of potential risk and focus their audit procedures accordingly.

4. Compliance with auditing standards

Auditing standards and regulations require auditors to obtain sufficient and appropriate evidence to support their opinions. Failing to do so can lead to legal and professional consequences.

The audit risk element

Audit risk refers to the possibility that a company’s internal systems still contain material errors or vulnerabilities, even if the auditor issues a favorable “clean” opinion. In simpler terms, it’s the chance that the auditor overlooks something crucial.

There are various categories of audit risk:

- Control risk: This arises when the client’s internal controls fail to identify or prevent potential significant errors.

- Detection risk: It pertains to the likelihood of a notable mistake going unnoticed during the audit procedures.

- Inherent risk: This is the inherent likelihood of a substantial error or misstatement before any risk-reducing controls are put in place.

One of the primary objectives of the audit team is to minimize the risk of overlooking significant errors. They achieve this by conducting more thorough checks and accumulating additional evidence during the audit process to diminish the chances of making mistakes.

Types of audit evidence

Audit evidence encompasses various forms that auditors employ to scrutinize an organization’s financial statements and internal control systems. Each type of evidence offers unique insights and contributes to the auditor’s ability to provide an accurate opinion.

Let’s delve further into these evidence types:

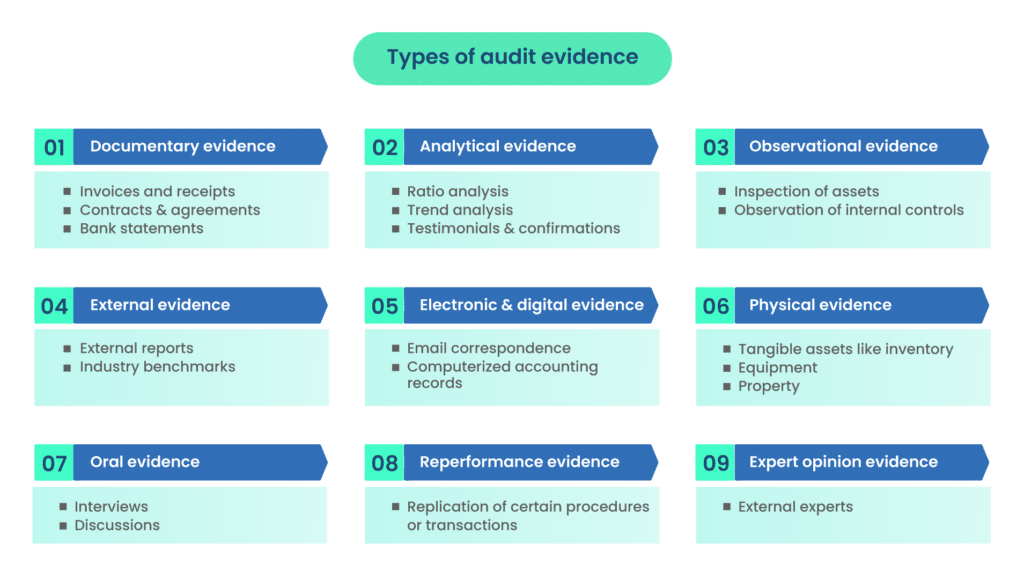

1. Documentary evidence

Documentary evidence is the most common type of audit evidence and typically includes written records and documents. It provides a tangible and often irrefutable source of information.

Some examples of documentary evidence include:

- Invoices and receipts: Invoices from suppliers, customer receipts, and other financial documents can be used to verify transactions, amounts, and the timing of financial events.

- Contracts and agreements: Contracts and agreements with suppliers, clients, employees, and other stakeholders can provide evidence of obligations, terms, and commitments that affect an organization’s financial statements.

- Bank statements: Bank statements and related documents offer critical evidence of cash balances, transactions, and bank reconciliations, helping auditors confirm the accuracy of an organization’s cash accounts.

Also read: Audit evidence: Ensuring accurate documentation and compliance

2. Analytical evidence

Analytical evidence involves the use of financial and non-financial data analysis to identify patterns, trends, anomalies, or unusual fluctuations that may indicate potential issues or areas of concern. Examples of analytical evidence include:

- Ratio analysis: Auditors often use financial ratios to assess the financial health and performance of a company. Ratios like liquidity ratios, profitability ratios, and leverage ratios provide valuable insights.

- Trend analysis: Comparing financial data over multiple periods to identify significant changes or anomalies can provide insights into potential risks or areas requiring further investigation.

- Testimonials and confirmations: Testimonials and confirmations involve obtaining written or oral statements from knowledgeable individuals, both within and outside the organization. These can include:

- Confirmation letters: Auditors may send confirmation letters to third parties, such as banks, customers, or suppliers, to independently verify balances, transactions, or other financial information.

- Expert opinions: Expert opinions from specialists or professionals in specific fields can provide evidence related to complex issues, such as the valuation of unique assets or liabilities.

3. Observational evidence

Observational evidence is gathered through direct observation and physical inspection. Auditors may use this type of evidence to assess the physical existence and condition of assets or the operation of internal controls. Examples include:

- Inspection of assets: Auditors may physically inspect inventory, property, or equipment to verify their existence and condition.

- Observation of internal controls: Auditors may observe internal control procedures in action to assess their effectiveness in preventing and detecting fraud or errors.

4. External evidence

External evidence is obtained from sources outside of the organization and can provide an independent perspective on financial information. Examples include:

- External reports: Credit ratings, market research reports, or industry-specific reports can provide external perspectives on an organization’s financial health and industry performance.

- Industry benchmarks: Comparing an organization’s performance against industry benchmarks or standards can provide valuable context for evaluating its financial position.

5. Electronic and digital evidence

In today’s digital age, electronic and digital evidence play a significant role in auditing. This includes information stored electronically and digitally, such as:

- Email correspondence: Emails and electronic communications can provide evidence of agreements, transactions, or decisions made by the organization.

- Computerized accounting records: Auditors often rely on digital accounting records, including ledgers, financial software, and databases, to gather evidence about an organization’s financial transactions and accounts.

6. Physical evidence

Sometimes, auditors need to go beyond documents and observe tangible assets. By physically inspecting items like inventory, equipment, or property, they can confirm their existence, condition, and valuation. For instance, in a manufacturing plant audit, auditors may physically count the inventory to reconcile it with the financial records.

7. Oral evidence

Interviews and discussions with individuals within the organization are essential for clarifying details, gathering explanations, and obtaining a deeper understanding of specific transactions or practices. Through dialogue with management, employees, and stakeholders, auditors gain valuable context for their assessments.

8. Re-performance evidence

To ensure the effectiveness of internal controls, auditors may replicate certain procedures or transactions performed by the organization. By reperforming these activities independently, they verify that controls are functioning as intended and that the organization’s practices align with its documented policies.

9. Expert opinion evidence

In complex or specialized areas, auditors may seek input from experts. These experts, often external to the audit firm, offer professional opinions based on their expertise. For instance, in the case of complex financial instruments, auditors may engage financial experts to assess their valuation.

Each of these evidence types has a specific role in the audit process. Auditors carefully select and combine these forms of evidence to ensure a comprehensive and accurate assessment.

Their judgment, expertise, and strategic use of evidence types are vital in delivering reliable audit opinions on an organization’s financial health and internal controls. The synergy of these evidence types enhances the audit’s credibility and trustworthiness.

Auditors must carefully select and combine these types of evidence to obtain sufficient and appropriate evidence to support their audit opinions and conclusions.

Evaluation of audit evidence

The evaluation of audit evidence is a critical step in the audit process. After auditors have gathered various types of evidence, they must assess its relevance and reliability to draw conclusions and form their audit opinions.

This evaluation includes the following key aspects:

1. Sufficiency of evidence

The sufficiency of evidence refers to whether the quantity of evidence obtained is adequate to support the audit objectives. Auditors must consider the following factors when assessing sufficiency:

- The size and complexity of the organization: Larger and more complex organizations typically require more extensive audit procedures and evidence.

- Materiality: Auditors should focus on areas and account balances that are more likely to contain material misstatements.

- Risk assessment: Higher levels of assessed risk may necessitate more extensive audit procedures and evidence to address potential misstatements.

2. Appropriateness of evidence

The appropriateness of evidence is determined by its relevance and reliability. Auditors must consider:

- Relevance: Evidence should be directly related to the assertions being tested and the audit objectives. Irrelevant evidence does not contribute meaningfully to the audit.

- Reliability: Reliable evidence is trustworthy and free from bias. Factors such as the source, the quality of internal controls, and the nature of the evidence influence its reliability.

3. Completeness of evidence

Auditors must ensure that they have gathered evidence from a wide range of sources and procedures to obtain a comprehensive view of the financial statements. The evidence collected should cover all significant areas and assertions, and any gaps should be addressed through additional procedures.

4. Reliability of audit evidence

The reliability of audit evidence is essential to ensuring that it is accurate, unbiased, and can be trusted for making informed decisions.

Factors affecting the reliability of evidence include:

a. Source reliability

The source of the evidence significantly influences its reliability. Internal sources, such as financial records generated by the organization itself, may be more reliable if the organization maintains robust internal controls. External sources, while often reliable, can vary in reliability based on the source’s reputation and independence.

b. Auditor’s independence

Auditors must maintain their independence and objectivity throughout the audit process. The more independent the auditor, the more reliable the evidence they gather. Independence helps prevent conflicts of interest and bias that could compromise the quality of the evidence.

c. External vs. internal evidence

External evidence, such as third-party confirmations or industry reports, is generally more reliable than internal evidence produced by the organization being audited. However, internal evidence can still be reliable if the organization has strong internal controls and processes in place to ensure data accuracy.

Special considerations in audit evidence

In some situations, auditors must apply special considerations when obtaining and evaluating audit evidence. These considerations are necessary to address unique challenges and risks that may arise during the audit process.

Key special considerations include:

1. Fraud detection and audit evidence

Auditors are responsible for detecting material misstatements resulting from fraud. Special audit procedures, including forensic audit techniques, may be employed to gather evidence of potential fraud. This involves a higher level of professional skepticism and scrutiny.

2. Going concern assumption and audit evidence

When assessing an entity’s ability to continue as a going concern, auditors must consider evidence related to the organization’s financial health and viability. Events or conditions that cast doubt on the going concern assumption may require the auditor to modify the audit opinion or include an explanatory paragraph in the audit report.

3. Audit evidence in a computerized environment

In today’s technology-driven world, auditors encounter unique challenges in gathering evidence from computerized systems. They must assess the integrity, accuracy, and reliability of electronic and digital evidence. The use of data analytics and advanced technologies may also play a significant role in obtaining audit evidence.

These special considerations highlight the need for auditors to adapt their audit procedures and evidence-gathering techniques to address specific risks and complexities in the audit environment.

By addressing these considerations, auditors can enhance the quality and relevance of the audit evidence obtained and provide more reliable audit opinions.

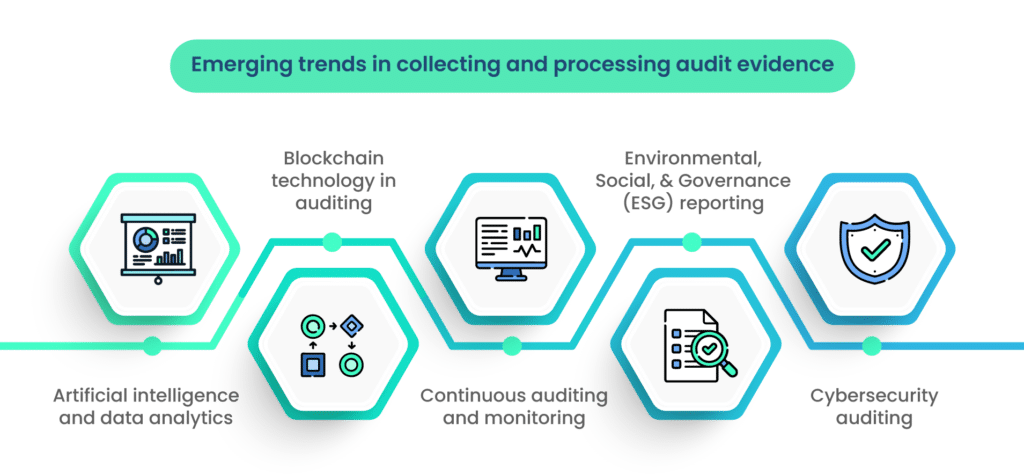

Emerging trends in collecting and processing audit evidence

The field of auditing is continually evolving, driven by technological advancements, changes in business practices, and regulatory developments. Several emerging trends in audit evidence are shaping the profession:

1. Artificial intelligence and data analytics

The use of artificial intelligence (AI) and data analytics is becoming increasingly prevalent in auditing. Auditors can leverage AI to process vast datasets and identify anomalies or patterns that may be indicative of fraud or errors. Data analytics can also provide more in-depth insights into financial performance and internal controls.

2. Blockchain technology in auditing

Blockchain technology, with its transparent and tamper-resistant ledger, has the potential to revolutionize auditing. It can provide a secure and immutable record of financial transactions and other critical data. Auditors are exploring how blockchain technology can be harnessed to enhance the reliability and integrity of audit evidence.

3. Continuous auditing and monitoring

Continuous auditing and monitoring involve real-time or near-real-time assessment of financial transactions and controls. This approach allows auditors to identify issues promptly rather than relying solely on periodic audits. It enhances the relevance and timeliness of audit evidence.

4. Environmental, Social, and Governance (ESG) reporting

As organizations place a greater emphasis on sustainability and responsible business practices, auditors are increasingly involved in auditing ESG data. Auditing ESG disclosures requires specialized knowledge and additional audit procedures to ensure the reliability of non-financial data.

5. Cybersecurity auditing

With the growing threat of cyberattacks and data breaches, cybersecurity auditing has become a critical area of focus. Auditors must assess the adequacy of an organization’s cybersecurity controls to protect sensitive data and financial information.

These emerging trends reflect the evolving landscape of audit evidence and the need for auditors to adapt to changing business environments and technologies.

Staying informed about these trends is crucial for auditors and audit firms to remain effective and relevant in the field. Auditors should be prepared to leverage new tools and methodologies to improve the quality and efficiency of their work.

Wrapping up: The ongoing evolution of audit evidence

The audit profession is dynamic, continually adapting to changes in technology, business practices, and regulatory requirements. Auditors must keep pace with these changes to remain effective in their roles.

As audit evidence evolves, so does the need for auditors to develop new skills and leverage technology to enhance the quality and relevance of the evidence they gather.

In conclusion, audit evidence is the cornerstone of the auditing process, providing the factual basis for forming opinions on financial statements and internal controls. By understanding the types, evaluation, and documentation of audit evidence, auditors can carry out their duties with integrity and professionalism.

Further, the evolving landscape of audit evidence, with its emphasis on technology and emerging trends, presents exciting opportunities and challenges for the audit profession. Staying informed and embracing these changes is crucial for auditors to continue to deliver value to their clients and stakeholders.

Audit evidence refers to the information and documentation that auditors collect and evaluate during an audit to support their conclusions about the financial statements. It plays a crucial role in auditing, as it helps auditors assess the fairness and accuracy of the financial information presented in those statements. Audit evidence provides a basis for the auditor’s opinion on whether the financial statements are free from material misstatements and can be relied upon by stakeholders.

Audit evidence can be categorized into several primary types, including: – Documentary evidence: This includes financial statements, invoices, contracts, and other written records. – Physical evidence: Tangible items like inventory, equipment, or property that auditors physically inspect. – Oral evidence: Information obtained through discussions and interviews with company personnel and third parties. – Analytical evidence: Data analysis and comparisons that help auditors identify patterns or anomalies. – External evidence: Information from external sources, such as bank statements, confirmations from third parties, or legal opinions. Auditors gather evidence through procedures like inspection, observation, inquiry, and confirmation, depending on the type of evidence and audit objectives.

Auditors use professional judgment to assess the reliability and sufficiency of audit evidence. They consider factors such as the source, nature, and reliability of the evidence. For instance, evidence obtained directly from an independent third party may be more reliable than evidence prepared by the entity being audited. The sufficiency of evidence depends on the audit risk and the materiality of the item being tested. Auditors aim to collect enough evidence to provide reasonable assurance that the financial statements are free from material misstatements.

Common types of audit evidence in financial audits include: – Bank statements and reconciliations – Invoices, purchase orders, and sales contracts – Payroll records and tax filings – Inventory counts and observations – Confirmation of balances with third parties – Minutes of meetings and board resolutions – Legal opinions and agreements – Financial reports and ledgers – Management representations and confirmations These forms of evidence are used to verify transactions, account balances, and the overall presentation of financial information in the statements.

Auditors encounter various challenges, including dealing with uncooperative or dishonest clients, complex transactions, and issues related to the availability and reliability of evidence. These challenges are addressed through professional skepticism, thorough audit planning, the use of specialized audit procedures when necessary, and adherence to ethical and professional standards. Auditors may also seek legal advice or engage specialists to address complex issues and ensure the quality of audit evidence. Clear communication with the client and professional skepticism in evaluating evidence help mitigate these challenges.