- SSAE 18 is the AICPA auditing standard that governs how SOC 1 and SOC 2 reports are produced and what service organizations must demonstrate to pass enterprise vendor reviews

- It introduced three requirements compliance teams still navigate today: formal vendor management programs, mandatory annual risk assessments, and subservice organization disclosures across all SOC engagements

- Genuine SSAE 18 readiness requires moving from annual audit preparation to continuous compliance, with automated evidence collection, vendor oversight workflows, and cross-team accountability built into daily operations

Enterprise trust has a new price of entry. It is no longer enough to point to a policy document or a checkbox audit from eighteen months ago.

Organizations that handle client data, process transactions, or provide outsourced services are increasingly measured against a more demanding standard: one that asks not just whether controls exist, but whether they operated consistently and how you can prove it.

According to Verizon’s 2025 Data Breach Investigations Report, the share of breaches involving a third party doubled in a single year, reaching 30%.

SSAE 18, published by the AICPA in 2016, is the auditing framework that formalized how service organizations are held accountable for those relationships. It is also the foundation on which every SOC 2 report your customers request is built.

It changed what enterprise buyers are entitled to expect from their service providers, raising expectations around vendor oversight, internal controls, and evidence in ways that still shape how procurement teams evaluate vendors today.

This article explains what SSAE 18 is, how it relates to SOC 2, what it requires of service organizations, where implementation gets difficult, and what building a genuinely continuous compliance program looks like in practice.

What is SSAE 18?

SSAE 18, or the Statement on Standards for Attestation Engagements No. 18, is the auditing standard published by the American Institute of Certified Public Accountants (AICPA) in April 2016, with most provisions becoming effective on May 1, 2017.

It governs how independent certified public accountants examine and report on a service organization’s internal controls, processes, and systems. If your customers are asking for a SOC 2 report, SSAE 18 is the standard the audit is conducted under.

The standard did not arrive without precedent. It replaced SSAE 16, which had itself superseded SAS 70, consolidating a fragmented set of prior attestation standards into a single clarified framework.

Each iteration raised the bar on what auditors were expected to examine and what service organizations were expected to demonstrate.

Under SSAE 18, both SOC 1 and SOC 2 reports are issued. SOC 1 reports address controls over financial reporting, while SOC 2 reports evaluate controls relevant to security, availability, processing integrity, confidentiality, and privacy.

The standard provides the rules of engagement that auditors follow when producing either report type, ensuring findings are consistent, reliable, and comparable across organizations.

What changed from SSAE 16 to SSAE 18

SSAE 18 was not a cosmetic update. Three operational changes distinguished it from its predecessor in ways that compliance teams still feel today.

- Service organizations were required to maintain a formal third-party vendor management program, which is documented, scoped, and backed by traceable evidence

- An annual risk assessment became mandatory, not merely encouraged, with a recurring, documented process reviewable by auditors

- Subservice organization disclosures, previously required only in SOC 2 reports, became mandatory across all SOC engagements

SSAE 18 also expanded what attestation engagements could cover, moving beyond financial controls to include compliance with laws, contractual arrangements, and agreed-upon procedures.

What is an SSAE 18 report?

An SSAE 18 report is any attestation report produced by an independent CPA firm under the SSAE 18 standard. In practice, this means a SOC 1, SOC 2, or SOC 3 report.

Within SOC 1 and SOC 2 engagements, two report structures exist:

- Type I evaluates whether controls are suitably designed at a specific point in time

- Type II assesses whether those controls operated effectively over a defined review period, typically between six and twelve months

Enterprise buyers almost always request Type II because it reflects sustained control performance, not a point-in-time snapshot.

Is SSAE 18 the same as SOC 2?

No. SSAE 18 is the auditing standard. SOC 2 is a report produced under that standard. They operate at different levels and serve different audiences.

SSAE 18 tells auditors how to conduct the engagement. SOC 2 tells stakeholders whether your security controls hold up. Think of it the way you would GAAP and a financial statement: one is the rulebook, the other is the output.

Most SaaS companies pursuing SOC 2 are already operating within the SSAE 18 ecosystem, whether they realize it or not. The standard governs the engagement; the report communicates the result.

Key SSAE 18 requirements modern companies cannot ignore

Enterprise buyers now ask pointed questions during procurement: who has access to their data, how vendors are monitored, and what happens between audits. The requirements below are what give your answers teeth.

1. Vendor oversight and subservice organization management

Under SSAE 18, vendor oversight is a documented, auditable obligation, not a procurement formality. Service organizations must:

- Maintain an updated inventory of subservice organizations, including cloud infrastructure providers, identity providers, payroll processors, ticketing systems, and development platforms

- Account for shadow IT and unauthorized AI tools that may be processing client data outside the documented control environment. Untracked tools are effectively unscoped subservice organizations, and auditors will treat them as gaps.

- Choose a disclosure method for each vendor: carve-out, where the auditor excludes a subservice organization’s controls from scope, or inclusive, where those controls are included and tested. The choice affects both the audit scope and the evidence your organization is responsible for producing.

- Document Complementary Subservice Organization Controls (CSOCs), which define how a subservice organization’s controls interact with and support your own control environment

- Review vendor SOC reports periodically throughout the year, not only at onboarding. A vendor whose certification lapses mid-period is an unresolved gap in your report.

2. Internal controls that operate continuously

In an SSAE 18 audit, a control that existed for ten months but lapsed in the eleventh shows up as an exception in a Type II report. Auditors test consistency across the full review period, not just at assessment time. Controls that must operate without interruption include:

- Access management

- Change management

- System monitoring and logging

- Incident response

- Evidence retention

3. Ongoing evidence collection

Manual screenshots become unreliable at scale. System-generated evidence is more defensible because it is timestamped, consistent, and difficult to reconstruct retroactively. Auditors increasingly expect:

- MFA enforcement logs

- GitHub branch protection records

- AWS configuration monitoring outputs

- HR offboarding and access revocation logs

Evidence gaps anywhere in the review period, even brief ones, create exceptions in the auditor’s report.

4. Accountability across teams

SSAE 18 does not implicate only the compliance function. Engineering, IT, security, HR, procurement, and leadership all own pieces of the control environment. A change management process sits with engineering.

Offboarding logs come from HR. MFA enforcement is an IT function. When compliance is treated as a siloed task rather than a cross-organizational discipline, gaps appear exactly where ownership is unclear.

Is SSAE 18 mandatory, and who actually needs it?

Nowhere in US law does a regulation mandate that service organizations undergo SSAE 18 attestation. The mandate comes from somewhere else entirely.

Organizations selling to enterprise buyers, operating in regulated industries, or handling sensitive client data will find SSAE 18 readiness effectively required.

Enterprise procurement teams routinely condition vendor approval on a SOC 2 Type II report, and those reports are issued under SSAE 18. For these organizations, an SSAE 18 audit is not optional in any practical sense.

Organizations most commonly in scope include:

- SaaS providers handling customer data

- Cloud service and infrastructure providers

- Fintech and payment processing platforms

- Healthcare vendors and health data processors

- Payroll and HR technology providers

- Managed service providers

- Enterprise technology vendors with B2B sales motions

If you are unsure whether your organization falls here, these signals are a reliable guide.

You likely need SSAE 18 readiness if:

- Enterprise customers are requesting SOC reports as part of vendor approval

- You handle financial transactions, health data, or personal information on behalf of clients

- You operate in a regulated industry or sell into one

- You are scaling toward a Series B raise or an enterprise market segment

- Your deals are stalling at the security review stage

The biggest SSAE 18 challenges for SaaS companies

Meeting SSAE 18 requirements on paper is one thing. Sustaining them operationally across a full audit period is another. These are the challenges compliance leads most commonly encounter.

1. Vendor sprawl

Most SaaS companies accumulate tools faster than they document them. By the time an audit window opens, the vendor inventory is outdated, approvals are informal, and several tools processing client data have never been reviewed.

Without a centralized vendor management process, SSAE 18’s oversight requirements are nearly impossible to satisfy consistently.

2. Manual evidence collection at scale

Screenshots and spreadsheets hold up for a Type I report. They begin to break under a twelve-month Type II review period. Logs go missing. Evidence is reconstructed after the fact.

Teams spend the weeks before an audit doing work that should have happened continuously. Manual methods do not scale to what SSAE 18 actually requires.

3. Controls drift between audits

Permissions change when someone joins or leaves. Infrastructure evolves with new deployments. Teams move fast, and controls that were in place in January may look different by September.

Readiness is not a project. It is a living system, and most compliance programs are not built to treat it that way.

4. Cross-functional ownership gaps

Who owns the MFA enforcement log? Who flags a vendor SOC report that lapses mid-period? Who updates the vendor inventory when a new tool gets provisioned? When answers to these questions are unclear, the gaps surface in auditor findings.

Engineering pushback, compliance fatigue, and dependency bottlenecks are symptoms of a program without defined ownership across teams.

5. The Type I to Type II gap

Knowing your controls exist and proving they operated consistently for twelve months are two entirely different operational problems. Many organizations pass a Type I report with relative ease, then discover that sustaining those controls without drift across a full review period requires a fundamentally different approach.

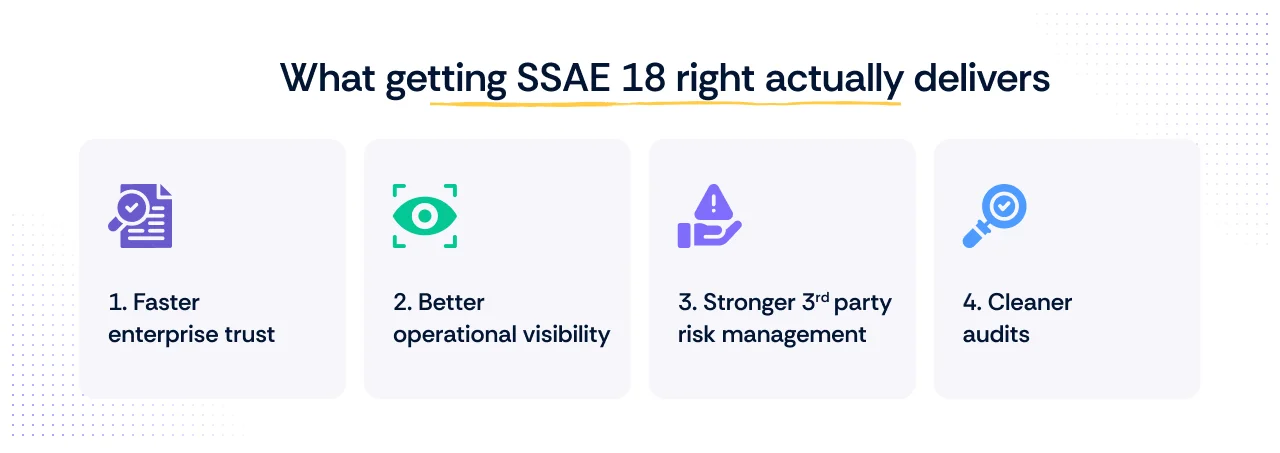

Benefits of SSAE 18 for modern organizations

The challenges in the previous section are real. But they are also solvable, and solving them has measurable operational outcomes beyond a passing audit report.

1. Faster enterprise trust

A well-maintained SOC 2 under SSAE 18 answers most vendor questionnaire questions before they are asked. For B2B companies competing on enterprise accounts, a clean Type II report on request is increasingly a competitive differentiator, not a compliance checkbox.

2. Better operational visibility

Continuous compliance gives compliance leads something point-in-time audits never could: a live view of the control environment. Issues surface earlier, get resolved faster, and rarely reach an auditor as findings.

3. Stronger third-party risk management

Documented vendor oversight builds an early warning system. Problems are caught internally before they become auditor findings or, worse, incidents that a customer discovers first.

4. Cleaner audits

Fewer exceptions, faster completion, lower CPA fees. The report reflects how the organization actually operates, not how it performed during a preparation sprint.

How modern SaaS companies operationalize SSAE 18 readiness

The gap between knowing what SSAE 18 requires and building a program that delivers it continuously is where most compliance teams struggle. The organizations that close that gap are not doing more auditing. They are doing less scrambling because readiness is built into their day-to-day operations.

From audit preparation to continuous compliance

The shift from annual preparation to continuous compliance is not a philosophical one. It is an architectural one. It requires:

- Automated evidence collection is mapped to control frameworks, running year-round rather than being activated before audit windows

- Vendor oversight workflows with renewal tracking and CSOC documentation, so no vendor report lapses without a flag

- Centralized controls with defined cross-team ownership, so the right person is accountable for the right evidence at all times

- Audit-ready evidence packaging that does not require reconstruction at assessment time

The practical principle: the best umbrellas are bought before it rains.

What continuous compliance looks like in practice

Each row represents a control area with a defined trigger, a documented evidence trail, and a clear decision path. This is what SSAE 18 audit readiness looks like when it is embedded into operations rather than bolted on before assessment time.

How Scrut helps in SSAE 18

Scrut Automation offers an AI platform powered by autonomous agents that operationalize continuous compliance and security. For teams managing SSAE 18 readiness, this means automated evidence collection mapped to control frameworks, continuous vendor oversight with renewal tracking, and audit-ready documentation that does not need to be reconstructed at assessment time.

The platform replaces audit chaos with scalable execution, enabling growing businesses to build trust at scale and manage cyber risk effectively.

Every item on the checklist above is something Scrut is built to track, automate, and keep current, not just before an audit, but across the entire compliance cycle.

See how Scrut works and get a personalized quote.

SSAE 18 is the attestation standard issued by the AICPA that defines how independent auditors assess and report on a service organization’s internal controls. Effective May 1, 2017, it underpins all SOC 1 and SOC 2 reports that enterprise buyers request from their vendors.

No, they serve different functions. SSAE 18 is the standard auditors follow when conducting an engagement. SOC 2 is the report that results from it. One sets the rules; the other documents the outcome.

The full name is Statement on Standards for Attestation Engagements No. 18. It was issued by the AICPA’s Auditing Standards Board in April 2016 and became effective on May 1, 2017, consolidating and superseding all prior SSAE standards into a single clarified framework.

No law requires it. However, service organizations selling to enterprise clients, handling sensitive data, or operating in regulated industries will find it commercially unavoidable. Enterprise buyers routinely require SOC 2 Type II reports as a condition of vendor approval, and those reports are conducted under SSAE 18.

SSAE 18 replaced SSAE 16, effective May 1, 2017. It consolidated prior attestation standards into a single framework and introduced stronger requirements around vendor oversight and risk assessment.

.png)