Choose risk-first compliance that’s always on, built for you.

Go back to blogs

Navigating PCI DSS compliance: A comprehensive checklist

Last updated on

min. read

Securing payment card data is paramount in the modern digital landscape. As financial transactions shift to digital platforms, ensuring the protection of payment card data becomes crucial to prevent fraud, maintain consumer trust, and mitigate the escalating threat of cyberattacks targeting sensitive financial information.

Between 2019 and 2021, the global circulation of payment cards witnessed a growth of more than two billion, with projections indicating a continued increase.

The Payment Card Industry Data Security Standard (PCI DSS) serves as the compass for organizations navigating this critical terrain. PCI DSS provides a standardized set of security measures and guidelines to protect cardholder data, ensuring secure transactions and reducing the risk of data breaches within the payment card industry.

In this blog, we present a comprehensive PCI DSS compliance checklist to guide businesses through the essential steps for ensuring the protection of sensitive cardholder information.

Understanding PCI DSS

The PCI DSS stands as a global framework designed to safeguard the integrity and confidentiality of payment card data.

Enacted to counter the escalating threats to financial transactions in the digital age, PCI DSS outlines a comprehensive set of security requirements and best practices that organizations must adhere to when handling payment card information.

Its significance lies in creating a standardized and robust security posture, ensuring that entities across the globe implement consistent measures to fortify their payment card environments against cyber threats.

PCI DSS holds universal applicability, transcending geographical boundaries to establish a common language for secure transactions worldwide. Its global adoption emphasizes the interconnected nature of the modern financial ecosystem, where seamless and secure transactions are paramount. By adhering to PCI DSS, organizations contribute to a collective effort to foster trust and confidence in the security of payment card transactions on a global scale.

This standard not only serves as a shield against potential data breaches but also underscores the collaborative responsibility of the payment card industry to uphold the highest standards of security, ultimately fortifying the foundation of secure digital transactions across diverse regions and industries.

Failing to adhere to PCI requirements may lead to significant repercussions. In the event of a data breach and subsequent investigations revealing non-compliance, fines may extend from $5,000 to $10,000 per month until compliance is achieved. Additionally, the potential reputational harm resulting from a data breach due to neglecting PCI DSS-recommended precautions should not be overlooked.

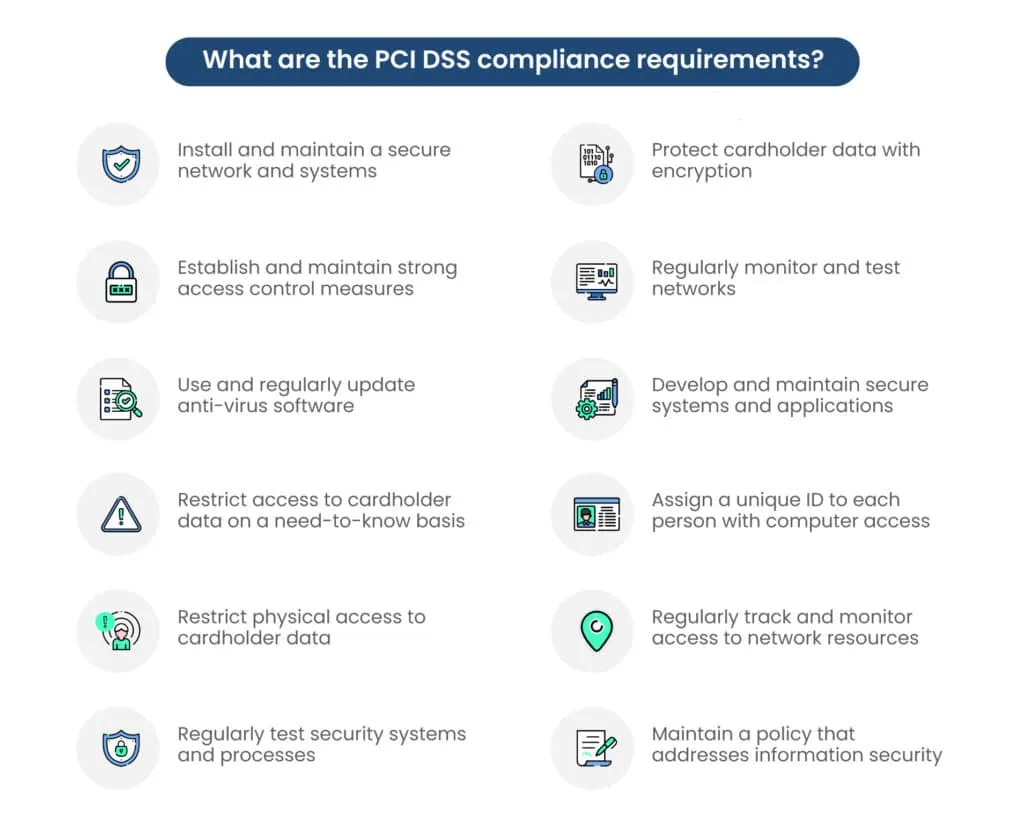

PCI DSS compliance requirements step-by-step

Here are the 12 requirements of PCI DSS:

1. Install and maintain a secure network and systems

- Implement robust security measures for network infrastructure.

- Regularly update and patch systems to address vulnerabilities.

2. Protect cardholder data with encryption

- Encrypt sensitive information during transmission and storage.

- Use strong encryption algorithms to safeguard cardholder data.

3. Establish and maintain strong access control measures

- Implement strict access controls based on the principle of least privilege.

- Authenticate and authorize individuals accessing cardholder data.

4. Regularly monitor and test networks

- Implement continuous monitoring to detect and respond to security incidents.

- Conduct regular penetration testing and vulnerability assessments.

5. Use and regularly update anti-virus software

- Deploy and maintain anti-virus software on all systems.

- Regularly update virus definitions to protect against new threats.

6. Develop and maintain secure systems and applications

- Follow secure coding practices for software development.

- Regularly update and patch applications to address security vulnerabilities.

7. Restrict access to cardholder data on a need-to-know basis

- Limit access to cardholder data to individuals who require it for their job roles.

- Implement strong authentication mechanisms for access.

8. Assign a unique ID to each person with computer access

- Ensure that each user has a unique identifier for system access.

- Maintain proper user account management and disable inactive accounts.

9. Restrict physical access to cardholder data

- Implement physical security measures to prevent unauthorized access to systems and data.

- Control and monitor physical access to data storage locations.

10. Regularly track and monitor access to network resources

- Implement logging mechanisms to track user activities and access.

- Regularly review and analyze logs to identify and respond to suspicious activities.

11. Regularly test security systems and processes

- Conduct regular security testing, including penetration testing and vulnerability assessments.

- Ensure that security measures and processes are effective and up-to-date.

12. Maintain a policy that addresses information security

- Establish and maintain an information security policy.

- Regularly review and update the policy to address emerging threats and changes in the business environment.

PCI DSS compliance checklist

To ensure seamless adherence to PCI DSS compliance requirements, organizations often rely on a comprehensive PCI DSS checklist.

This PCI DSS audit checklist serves as a systematic guide, encompassing key elements that businesses must assess and implement to meet the stringent security standards set by the PCI DSS.

This checklist should be adapted to the specific requirements and nuances of individual business environments.

1. Scope identification

- Define Cardholder Data Environment (CDE): Clearly outline and understand the boundaries of your Cardholder Data Environment, encompassing all systems, networks, and processes that store, process, or transmit cardholder data. This includes not only databases and applications but also any third-party systems connected to the cardholder data flow.

- Segmentation and isolation: Implement network segmentation to isolate the CDE from other non-payment systems. This limits the scope of PCI DSS requirements, making compliance efforts more focused and efficient.

- Identify data flows: Map the flow of cardholder data throughout your organization, from point of entry to storage and eventual disposal. Understand how data moves across different systems and ensure that all these touchpoints are included in the defined scope.

- Third-party inclusion: If third-party service providers have access to cardholder data, ensure their systems and processes are also within the scope. This involves assessing and validating the security measures implemented by these external entities.

- Regularly review and update: The CDE is dynamic, and changes in systems or processes can impact its scope. Regularly review and update the defined scope to accommodate any changes in the organization's infrastructure or business processes. This ongoing assessment ensures that the scope remains accurate and reflective of the current environment.

2. Conducting a risk assessment

- Identify and prioritize risks: Conduct a thorough risk assessment to identify potential vulnerabilities and threats to cardholder data within the defined scope. Prioritize risks based on their likelihood and potential impact on the security of payment card information.

- Assess impact and likelihood: Evaluate the potential impact of identified risks on the confidentiality, integrity, and availability of cardholder data. Additionally, assess the likelihood of these risks materializing, taking into account current security controls and mitigation measures.

- Document findings: Document the findings of the risk assessment, including identified vulnerabilities, potential threats, and their corresponding risk levels. This documentation serves as a foundation for developing risk mitigation strategies and informs decision-making throughout the compliance process.

- Risk mitigation strategies: Develop and implement risk mitigation strategies to address identified vulnerabilities and threats. These strategies may include the enhancement of security controls, the implementation of new safeguards, or changes to existing processes to reduce the overall risk level.

- Regular review and update: The risk landscape is dynamic, with new threats emerging and business environments evolving. Regularly review and update the risk assessment to ensure it remains aligned with the organization's changing circumstances. This iterative process allows for ongoing risk management and enhances the organization's ability to adapt to evolving security challenges.

3. Implementing security policies

- Establish comprehensive security policies: Develop and document comprehensive security policies that align with PCI DSS requirements. These policies should provide clear guidelines and standards for protecting cardholder data and maintaining a secure environment.

- Cover key security areas: Ensure that security policies cover key areas such as access controls, encryption, network security, and incident response. Address each requirement of PCI DSS in a detailed and specific manner to guide employees and stakeholders in complying with security standards.

- Communicate policies across the organization: Disseminate security policies throughout the organization to ensure that all relevant personnel are aware of and understand the established security standards. This involves conducting training sessions, distributing written materials, and incorporating policies into the employee onboarding process.

- Regularly review and update: Security threats and technologies evolve over time. Regularly review and update security policies to reflect changes in the threat landscape, the organization's infrastructure, and the regulatory environment. This ensures that security measures remain effective and aligned with the latest industry best practices.

- Enforce compliance: Establish mechanisms to enforce compliance with security policies. This includes monitoring and auditing processes to ensure that employees and stakeholders adhere to the defined security standards. Enforcing compliance contributes to the consistent application of security measures across the organization.

4. Securing network infrastructure

- Implement strong network security measures: Strengthen your organization's network security by implementing robust measures such as firewalls, intrusion detection/prevention systems, and secure configurations. These measures contribute to creating a resilient defense against unauthorized access and potential threats to cardholder data.

- Network segmentation: Isolate the Cardholder Data Environment (CDE) through network segmentation. This ensures that systems storing or processing cardholder data are separate from non-payment systems, reducing the overall scope of PCI DSS compliance and enhancing the security of sensitive information.

- Regularly monitor and update: Establish continuous monitoring mechanisms to track network activity, detect anomalies, and respond promptly to potential security incidents. Regularly update and patch systems to address vulnerabilities and adapt to emerging threats, maintaining a proactive approach to network security.

- Access control measures: Implement stringent access controls for network resources, ensuring that only authorized individuals have access to sensitive information. Regularly review and update user access permissions to align with the principle of least privilege, limiting access to what is necessary for job functions.

- Secure configuration management: Enforce secure configurations for network devices, servers, and applications. Follow industry best practices and vendor guidelines to ensure that systems are configured securely, reducing the risk of exploitation by malicious actors. Regularly assess and update configurations to maintain a robust security posture.

5. Protecting cardholder data

- Utilize encryption and tokenization: Implement strong encryption and tokenization mechanisms to protect cardholder data throughout its lifecycle. Encryption ensures that sensitive information is transformed into unreadable formats, while tokenization replaces cardholder data with unique tokens, reducing the risk of exposure in the event of a breach.

- Mask sensitive information: Employ data masking techniques to conceal sensitive information within the organization. This adds an additional layer of protection, particularly during processes where access to the full cardholder data is not essential for legitimate business functions.

- Control access to stored data: Limit access to stored cardholder data to only those individuals who require it for their specific job roles. Enforce strict access controls, incorporating the principle of least privilege to minimize the risk of unauthorized access or internal threats.

- Regularly review and update security measures: Periodically review and update encryption, tokenization, and data masking measures to align with evolving security standards and technological advancements. This proactive approach ensures that cardholder data remains protected against emerging threats.

- Secure transmission of data: Implement secure methods for transmitting cardholder data, such as encrypted channels and secure protocols. This safeguards information during transit, preventing interception and unauthorized access by malicious entities attempting to exploit vulnerabilities in communication channels.

6. Access controls

- Enforce strict access controls: Implement and enforce access controls to restrict access to cardholder data based on the principle of least privilege. This ensures that individuals have access only to the information necessary for their specific job responsibilities, minimizing the risk of unauthorized access.

- Regularly review and update user access permissions: Conduct regular reviews of user access permissions to cardholder data. This includes removing access for individuals who no longer require it and updating permissions to reflect changes in job roles or responsibilities. Regular reviews contribute to maintaining a secure and well-regulated access environment.

- Authentication measures: Implement strong authentication measures, such as multi-factor authentication, to enhance the verification process for individuals accessing cardholder data. Multi-factor authentication adds an additional layer of security, requiring users to provide multiple forms of identification before gaining access.

- Access monitoring and logging: Implement robust monitoring and logging mechanisms to track access to cardholder data. Regularly review access logs to detect and respond to any suspicious activities or unauthorized access attempts promptly. Monitoring access contributes to maintaining a vigilant security posture.

- Education and awareness: Provide education and awareness programs for employees regarding access controls and the importance of securing cardholder data. Ensure that employees understand their role in maintaining secure access and report any unusual activities promptly. Education fosters a culture of security awareness within the organization.

7. Regular monitoring and testing

- Continuous monitoring: Establish continuous monitoring mechanisms to actively track security controls, network activities, and potential threats. This ongoing surveillance allows for the timely identification of anomalies or security incidents, enabling prompt response and mitigation.

- Vulnerability assessments: Conduct regular vulnerability assessments to identify weaknesses in systems, applications, and processes that could be exploited by attackers. Addressing vulnerabilities promptly is crucial for maintaining a robust security posture and reducing the risk of unauthorized access.

- Penetration testing: Periodically perform penetration testing to simulate real-world cyber-attacks and assess the effectiveness of security controls. This proactive testing helps identify potential weaknesses that might not be apparent through other means, allowing organizations to strengthen their defenses.

- Access log monitoring: Regularly review access logs and security event logs to detect and investigate any unusual activities or signs of unauthorized access. Log monitoring provides insights into the security status of systems and aids in the identification of potential security incidents.

- Incident response testing: Test the incident response plan through simulated exercises to ensure that the organization is well-prepared to handle security incidents. These tests should involve key personnel and assess the effectiveness of communication, coordination, and mitigation strategies during a simulated incident.

8. Incident response and reporting

- Develop an incident response plan: Create a comprehensive incident response plan outlining the steps to be taken in the event of a security incident involving cardholder data. Clearly define roles and responsibilities, communication channels, and escalation procedures.

- Personnel training: Train relevant personnel on the incident response plan to ensure a coordinated and effective response to security incidents. Regular training sessions help personnel understand their roles and responsibilities, fostering a proactive and well-prepared response.

- Establish clear reporting channels: Define clear reporting channels for employees to quickly and efficiently report any suspicious activities or potential security incidents. Rapid reporting is essential for the swift identification and containment of security threats.

- Incident investigation: Develop procedures for investigating security incidents, including the analysis of access logs, system alerts, and other relevant data. Thorough investigations help determine the scope of the incident, identify the root cause, and inform appropriate remediation measures.

- Regular review and update: Periodically review and update the incident response plan to incorporate lessons learned from simulated exercises and real incidents. An agile and adaptive incident response plan ensures continual improvement and effectiveness in the face of evolving security challenges.

9. Vendor management

- Assess third-party security practices: Evaluate the security practices of third-party vendors who have access to or handle cardholder data. Ensure that these vendors adhere to PCI DSS requirements and maintain robust security measures to protect sensitive information.

- Include security requirements in contracts: Establish contractual agreements with third-party vendors that clearly outline security requirements and expectations. These contracts should emphasize the importance of maintaining the confidentiality and integrity of cardholder data.

- Regularly monitor vendor compliance: Implement a regular monitoring process to ensure ongoing compliance with security requirements by third-party vendors. This involves conducting periodic assessments, audits, or reviews of their security practices.

- Incident response coordination: Collaborate with third-party vendors on incident response planning. Ensure that vendors are prepared to respond effectively to security incidents involving cardholder data, aligning their incident response capabilities with the organization's expectations.

- Review and update vendor agreements: Regularly review and update vendor agreements to reflect changes in security standards, business relationships, or regulatory requirements. Keeping agreements current ensures that security expectations remain aligned with evolving circumstances.

10. Compliance reporting

- Compile compliance reports: Regularly compile and submit compliance reports as required by PCI DSS. Ensure that these reports accurately reflect the organization's adherence to the established security standards and provide evidence of compliance.

- Maintain documentation: Keep comprehensive documentation of all compliance efforts, assessments, and validation results. Well-maintained documentation serves as a record of the organization's commitment to maintaining a secure environment and facilitates the audit process.

- Address non-compliance issues: Promptly address any identified non-compliance issues and take corrective actions. This involves implementing changes to security controls, policies, or processes to align with PCI DSS requirements and prevent recurrence of non-compliance.

- Regular internal audits: Conduct regular internal audits to assess the organization's ongoing compliance with PCI DSS. Internal audits help identify areas for improvement, validate the effectiveness of security measures, and ensure continuous alignment with the standard.

- Prepare for external audits: Be prepared for external audits by maintaining up-to-date documentation, evidence of compliance, and a thorough understanding of the organization's security posture. A proactive approach facilitates a smoother external audit process and demonstrates a commitment to maintaining PCI DSS compliance.

11. Employee training

- Educate employees on PCI DSS requirements: Provide comprehensive training for employees to ensure a clear understanding of PCI DSS requirements and their role in maintaining compliance. This includes awareness of security policies, access controls, and the significance of protecting cardholder data.

- Regular training sessions: Conduct regular training sessions to keep employees informed about evolving security threats, updates to PCI DSS standards, and changes in organizational policies. Ongoing education fosters a culture of security awareness and accountability among staff.

- Phishing awareness programs: Implement phishing awareness programs to educate employees on recognizing and mitigating phishing attacks. Since social engineering is a common tactic used by cybercriminals, employees should be vigilant and equipped to identify potential threats.

- Security incident reporting training: Train employees on the proper procedures for reporting security incidents promptly. This includes clear guidance on who to contact, what information to provide, and the importance of swift reporting to mitigate potential risks.

- Assessment of training effectiveness: Periodically assess the effectiveness of employee training programs by conducting evaluations, quizzes, or simulated exercises. This ensures that employees retain crucial knowledge and are well-prepared to contribute to the organization's overall security posture.

12. Physical security

- Control physical access to facilities: Implement measures to control and restrict physical access to facilities where cardholder data is processed, stored, or transmitted. This includes secure entry points, access cards, and surveillance systems to prevent unauthorized individuals from gaining physical access.

- Secure storage of physical assets: Safeguard physical assets such as servers, terminals, and devices that handle cardholder data. Ensure these assets are stored in secure locations with limited access, protecting them from theft, tampering, or unauthorized use.

- Monitor physical access: Establish monitoring mechanisms, such as security cameras and access logs, to track and record physical access to sensitive areas. Regularly review these logs to detect and respond to any suspicious activities or unauthorized entry.

- Employee awareness of physical security: Educate employees about the importance of physical security measures and their role in maintaining a secure environment. This includes promoting the awareness of badge protocols, reporting lost or stolen access cards, and recognizing and reporting unfamiliar individuals.

- Regular security audits: Conduct regular security audits of physical security measures to assess their effectiveness and identify areas for improvement. Physical security audits help ensure that controls are consistently enforced and aligned with PCI DSS requirements.

Wrapping up

In the ever-evolving landscape of digital transactions, PCI DSS compliance stands as a linchpin in securing payment card data. By diligently following this comprehensive checklist, organizations can not only meet compliance requirements but also fortify their defenses, instilling confidence in customers and stakeholders alike.

Get in touch with Scrut and embrace the commitment to safeguarding cardholder information, and navigate the path to PCI DSS compliance with confidence and precision.

Frequently Asked Questions

1. What is the primary purpose of PCI DSS compliance? The primary purpose of PCI DSS compliance is to establish and maintain a secure environment for handling payment card information. It sets standards and requirements to ensure the confidentiality and integrity of cardholder data, ultimately reducing the risk of data breaches and securing electronic payment transactions.

2. How can organizations determine the scope of their Cardholder Data Environment (CDE)? Organizations can determine the scope of their CDE by identifying all systems and processes that handle cardholder data. This involves understanding where payment card data is stored, processed, and transmitted within the organization. A clear understanding of the CDE is essential for effective compliance efforts.

3. What security measures should be implemented to protect cardholder data in accordance with PCI DSS? PCI DSS requires the implementation of various security measures, including encryption, access controls, network security, and regular monitoring. These measures aim to protect cardholder data throughout its lifecycle, from collection to storage and transmission.

4. What steps are involved in conducting a PCI DSS risk assessment? Conducting a PCI DSS risk assessment involves identifying potential vulnerabilities and threats to the cardholder data environment. Organizations must assess the potential impact of security incidents and prioritize risk mitigation strategies. This process helps in understanding and addressing security risks effectively.

5. How does PCI DSS compliance impact third-party vendor relationships? PCI DSS compliance extends to third-party vendors that have access to cardholder data. Organizations must assess the security practices of their vendors, ensure compliance with PCI DSS requirements, and establish contractual agreements that prioritize data security. The HIPAA Omnibus Rule holds business associates directly accountable for compliance, emphasizing the importance of understanding covered entities for overall adherence.

Table of contents

Related Posts